Deferred Income Annuity

Deferred income annuities are designed to bridge an income gap and maintain an income floor to cover basic expenses in retirement.

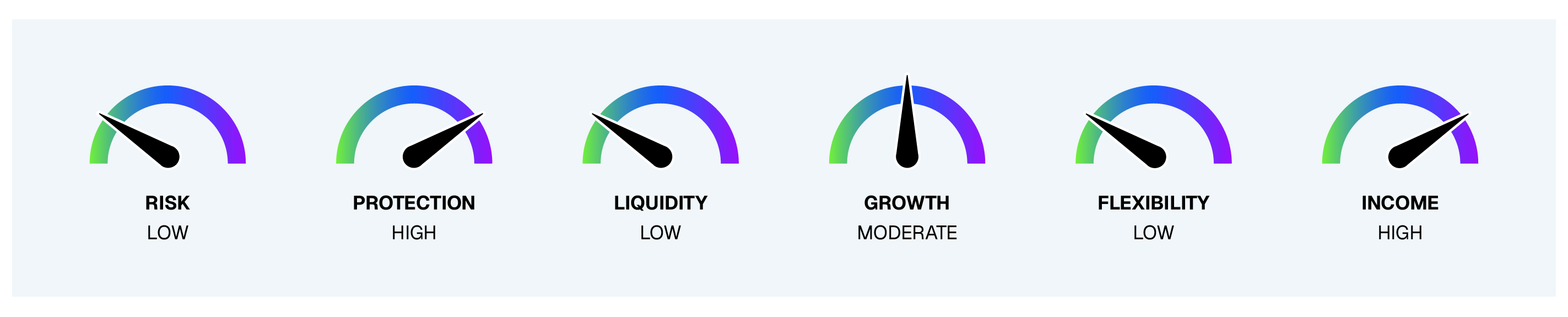

Deferred Income Annuity (DIA)

Investor Risk Profile: Low

Protection Level Provided: High

Funding Sources: Qualified retirement accounts, like a 401(k) or IRA

Deferred income annuities (DIAs) are designed to bridge an income gap and maintain an income floor to cover basic expenses in retirement. Funded through a lump-sum payment, or premium, in exchange for payments at a later date, DIAs can serve as a “personal pension,” providing an income stream for investors without a defined benefit plan through their employer.

Consider a DIA when your client needs:

Guaranteed Lifetime Income: DIAs are designed to manage longevity risk by generating an income stream that clients cannot outlive.

Deferred Income: These highly customizable products provide the annuitant with income payments (monthly, quarterly, or yearly) for life or a defined period, based on the annuity payout options.

Tax Relief Potential: If a DIA acts as a qualified longevity annuity contract (QLAC), it can help the owner delay required minimum distributions (RMDs), potentially lowering their tax burden.

Disclosures:

The purchase of an annuity within a retirement plan that already provides tax deferral under sections of the Internal Revenue Code results in no additional tax benefits. An annuity should be used to fund a qualified plan based upon the annuity’s features other than tax deferral. All annuity features, risks, limitations, and costs should be considered prior to recommending the purchase of an annuity within a tax-qualified retirement plan. In addition to surrender charges, withdrawals are subject to income tax.

Withdrawals prior to age 59 1/2 may also be subject to a 10% federal tax penalty.

Contact Us

Have more questions about our insurance offering? Call us at 888.327.0049 to speak to a DPL Consultant.