Get an Early Start: New Tax Changes Could Impact Year-End Planning

As the autumn air turns crisp, it’s a good time to think about year-end financial planning. With the passage of the One Big Beautiful Bill Act (OBBBA) and its sweeping changes to federal tax rules, it’s more important than ever to understand the tax-saving opportunities available to you. Strategic financial planning— including the use of vehicles like commission-free annuities—can help you manage your finances and navigate this new tax environment.

The New Tax Landscape and the OBBBA1

The new law includes key changes that could impact taxpayers of all ages. These include:

- Making provisions from the Tax Cuts and Jobs Act of 2017 permanent, including federal marginal tax rates and mortgage interest deduction rates

- Increasing the cap on state and local tax (SALT) deductions to $40,000 from $10,000

- Introducing an enhanced deduction for qualifying taxpayers 65 or older in addition to the standard or itemized deductions

- Allowing taxpayers who claim the standard deduction to also deduct qualified charitable donations, beginning in tax year 2026

- Implementing new limits on the deductions for gambling losses, also starting in tax year 2026

Many of the OBBBA provisions are tied to a taxpayer’s modified adjusted gross income, or MAGI. In simple terms, MAGI is your adjusted gross income with certain tax deductions and exemptions added back in. The IRS uses this more comprehensive income figure to determine eligibility for certain tax benefits.

Because the taxable income from an annuity can be controlled or deferred, it can be a useful tool for managing your MAGI and potentially qualifying for these new benefits.

Commission-free annuities can help you manage your modified adjusted gross income (MAGI) and secure new tax benefits

Begin with a Series of Questions

A great way to start planning is to ask yourself some standard questions. While these questions should be asked every year, the answers may have changed with the enactment of the OBBBA.

1. How can I minimize my 2025 taxes?

One approach to year-end planning starts by identifying the tax-saving and income-generating opportunities that are available for 2025. They may include:

- Funding retirement accounts (e.g., 401(k), IRA)

- Accelerating business deductions

- Initiating a Roth IRA conversion

- Implementing charitable giving strategies

- Strategically bunching donations like charitable donations or SALT payments (for example, paying the current and following year property tax bill in 2025.

- Executing wealth transfers through gifting

In addition, taxpayers who rely on portfolio-generated income may want to review their year-to-date distributions. Consider whether taking a December payment will adversely affect their overall tax picture.

2. What tasks need to be completed by the end of the year?

Required Minimum Distributions (RMDs)

Many retirees, as well as anyone who inherited an IRA in recent years, will need to take RMDs before the end of the year. Retirees with multiple IRA accounts should also inquire about which account or accounts they should tap for these distributions. Provisions of the existing SECURE Act create opportunities to make income annuities part of your RMD strategy.

Portfolio Review and Rebalancing

Year-end is the ideal time to review investment portfolios and rebalance assets, if necessary. Investors whose portfolios have grown during the recent bull market may be concerned about market volatility and the possibility of a downturn.

Annuities are often an important part of an asset protection strategy. For example, if you are concerned about preserving current gains, consider moving them out of the stock market and into a multi-year guaranteed annuity (MYGA). Alternatively, you could roll some portfolio assets into a registered index-linked annuity (RILA), which offers exposure to equity markets but with protection against a downturn.

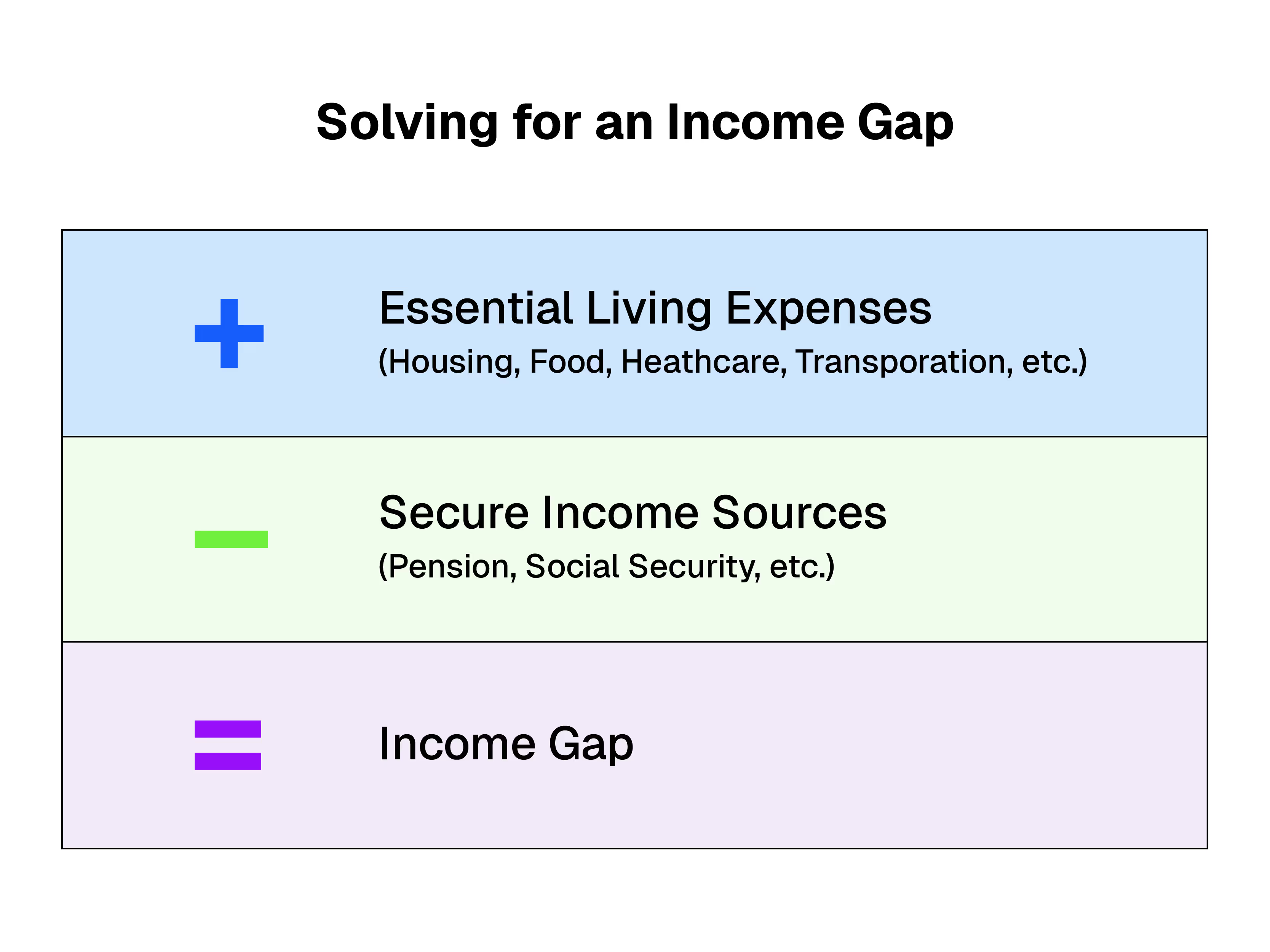

3. How much income will I need in 2026 and beyond?

If you depend on your investments to generate income, speak with your financial advisor to estimate how much income your portfolio must generate next year. If there is an income gap, an annuity might help close it.

If you are unfamiliar with annuities, they are insurance products uniquely designed to provide guaranteed income for life. Modern, commission-free annuities offer lower costs and improved benefits for consumers. Ask your financial advisor about the advantages of commission-free annuities and the protections they provide.

Year-end planning season is here. Talk with your financial advisor and/or tax professional about how to minimize taxes and position for success in the year ahead and if an annuity or insurance solution can help. You can also explore low-cost annuities that provide guaranteed income to see if this may be a good option to help you meet a retirement income need.

[press-a-contact-location]

1 “One Big Beautiful Big Act Provisions.” Internal Revenue Service. www.irs.gov.

.avif)