How to Generate Guaranteed Lifetime Income

Guaranteed lifetime income can play a valuable role in a retirement plan, providing a predictable and secure stream of income, and peace of mind that you’ll have funds you can count on for the rest of your life.

Three primary sources of guaranteed income for retirees are Social Security, pensions, and annuities.

But many of today’s retirees face challenges:

- Fewer than 2 in 10 Americans say they are very confident in the solvency of the Social security program

- Traditional pensions are increasingly rare as employers have moved away from “defined benefit” plans, that pay guaranteed benefits, to “defined contribution” plans like 401ks

- The burden of retirement funding now falls heavily on the individual

As a result, it's not surprising annuity sales are surging.

The vast majority of consumers believe that having guaranteed lifetime income in addition to Social Security in retirement is valuable, and annuities are products uniquely designed to deliver guaranteed income.*

“Think of an annuity as a personal pension that provides a paycheck every month in retirement for as long as you live,” says Willie Jones, a consultant at DPL Financial Partners, who works with consumers to help them generate income using annuities.

Learn more about guaranteed lifetime income.

Generating Guaranteed Lifetime Income Using Annuities

There are several types of annuities that can be used to generate guaranteed lifetime income, each with distinct benefits and features.

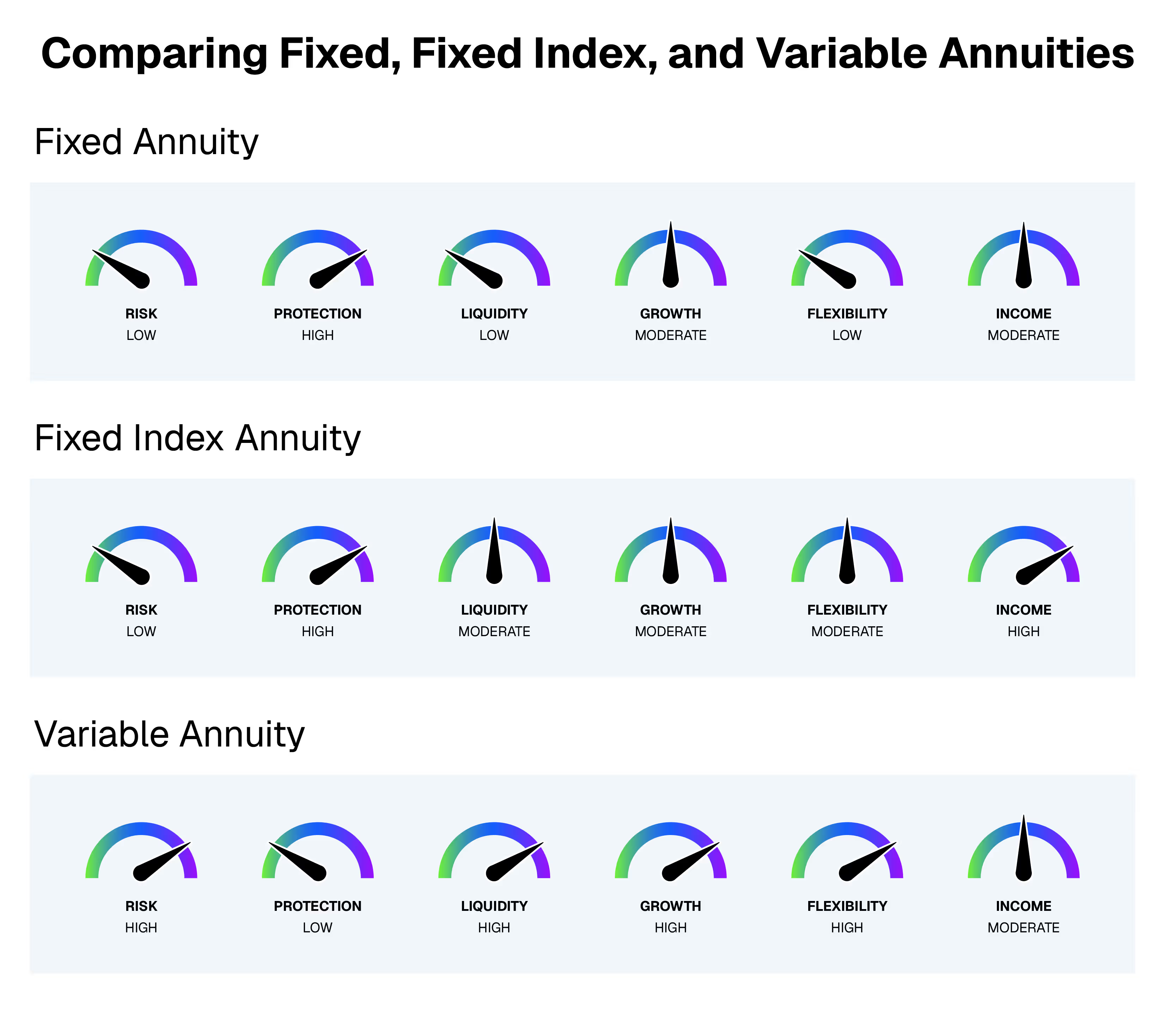

Three popular options are fixed annuities, fixed index annuities, and variable annuities.

Fixed annuities

A fixed annuity is a straightforward product like a CD, however, it is issued by an insurance company rather than a bank.

In a fixed annuity, you pay a lump sum that is invested in conservative, low-risk assets such as bonds or fixed-income securities. The insurance company pays a guaranteed fixed interest rate on your money, providing you with a predictable return over the agreed-upon term, which can range from two to ten years.

One of the benefits of a fixed annuity is your assets grow tax deferred, maximizing your earnings, until they're withdrawn at the end of the term. Or you can renew and let your money continue to grow.

Fixed index annuities

Fixed index annuities complete asset protection similar to a fixed annuity, however the returns are linked to the performance of a specific stock market index, like the S&P 500, providing the potential for higher returns.

Many FIAs offer optional guaranteed lifetime income riders for an additional cost. Using a rider, you can get a guaranteed income stream for life, deciding when you want to start receiving income and how often.

Depending on the product you choose, you also may be able to withdraw a portion of the annuity assets without paying a penalty charge, commonly referred to as a surrender fee.

“Fixed index or fixed annuities are very safe methods that basically protect your principal, so you have no losses,” says Jones. “They’re a good strategy for safety and peace of mind.”

Variable annuities

Variable annuities enable you to potentially earn higher returns but, unlike fixed and fixed index annuities, there is the potential to lose money in a market downturn.

Variable annuities offer a range of investment options and your returns are dependent on the performance of these underlying investments. Like fixed index annuities, many variable annuities offer income riders for an additional cost, enabling you to turn the accumulated assets into income that is guaranteed for your lifetime.

Learn more about the basics of annuities and how they work.

Why Consumers Value Annuities

Safety and peace of mind are two of the reasons consumers choose annuities.

According to the Alliance or Lifetime Income, people who are protected by guaranteed income from an annuity have a significantly more positive outlook on their retirement prospects.

"Guaranteed income makes people happier because it allows them to spend the money they have saved without having to worry about running out,” says Michael Finke, retirement professor & Frank M. Engle Chair of Economic Security at The American College in this DPL podcast.

The Evolution of Annuities

In the past several years, annuities have changed.

Traditional annuities are commission-based, meaning a salesperson is paid a commission to sell the products. Commissions drive up product costs, add complexity, and can erode benefits.

Modern annuities are commission-free, offering:

- Lower costs

- Greater transparency

- Improved benefits to consumers

These simplified products are built to deliver better value and a buying experience you control, vs. a sales process a salesperson controls.

Key Considerations

Some things to think about when considering how to generate guaranteed lifetime income for your retirement include your individual circumstances and your income needs to fund your desired lifestyle after you retire.

Individual Circumstances

Factors such as your retirement age, life expectancy, financial goals, and overall financial situation are important when considering if and how to source guaranteed lifetime income.

For example, when do you plan to retire? How long do you think you, and your spouse if you’re married, will live, and where do you want to live? What is your health status? Do you have goals for leaving a legacy? What are your available sources of income to fund your retirement?

The answers to these questions are critical to determining if guaranteed lifetime income is right for you, and the best way to generate it.

Income Needs

When considering how to generate guaranteed lifetime income, a good place to start is by determining how much your essential living expenses will be after you retire, like housing, food, clothing, etc.

Guaranteed income from an annuity is often used to help fund these expenses, giving you peace of mind that you’ll have money to meet your essential needs no matter how long you live.

Another benefit of using guaranteed lifetime income to cover your essential expenses in retirement is the flexibility to invest the rest of your portfolio more aggressively for growth and discretionary spending, without worrying that a market downturn will impact your ability to pay your bills.

By adding up your anticipated living expenses, then subtracting anticipated income from other sources like Social Security and/or a pension, you can arrive at the income gap to fill with an annuity. You then can determine how much money you would need to put into an annuity and what type of annuity is best suited to meet the income need.

TIP: A helpful tool is the Guaranteed Income Analysis. With a few inputs, you can see commission-free annuity options, with costs and benefits, that can meet your income need.

Inflation Adjustments

Inflation is a fact of life, and retirement, and an effective income strategy will consider the rising cost of living.

Some annuities offer income options that include a cost-of-living adjustment (COLA), which can help maintain purchasing power over the course of your retirement.

Says DPL’s Willie Jones, “As the cost of good goes up, we need more income to cover our basic expenses. And commission-free annuities can offer that.”

Getting Started with Guaranteed Lifetime Income

Annuities are powerful tools that are uniquely designed to generate guarantee lifetime income. And, now, modern, commission-free annuities are available without commissions, offering lower costs and improved benefits for consumers.

[press-a-contact-location]

*Guarantees are based on the claims paying ability of the issuing insurance company.

**Fixed index annuities are tax-deferred insurance products that provide market upside, while protecting principal from market losses. Assets are allocated into indices that are designed to replicate market performance. These fixed index annuity indices are typically accompanied with cap rates, spreads, or participation rates. Variable annuities involve risk, including possible loss of principal. All guarantees are based on the claims paying ability of the issuing insurance company.

.avif)