The 4% Rule and Annuities for Income

Planning for a financially secure retirement involves making informed decisions about how to source sustainable income. The 4% Rule is a popular rule of thumb used to determine how much retirees can safely withdraw each year from their investments portfolios to support their retirement spending. In this post, we’ll explore the 4% Rule and annuities and how each can play a role in your retirement income strategy.

What Is the 4% Rule

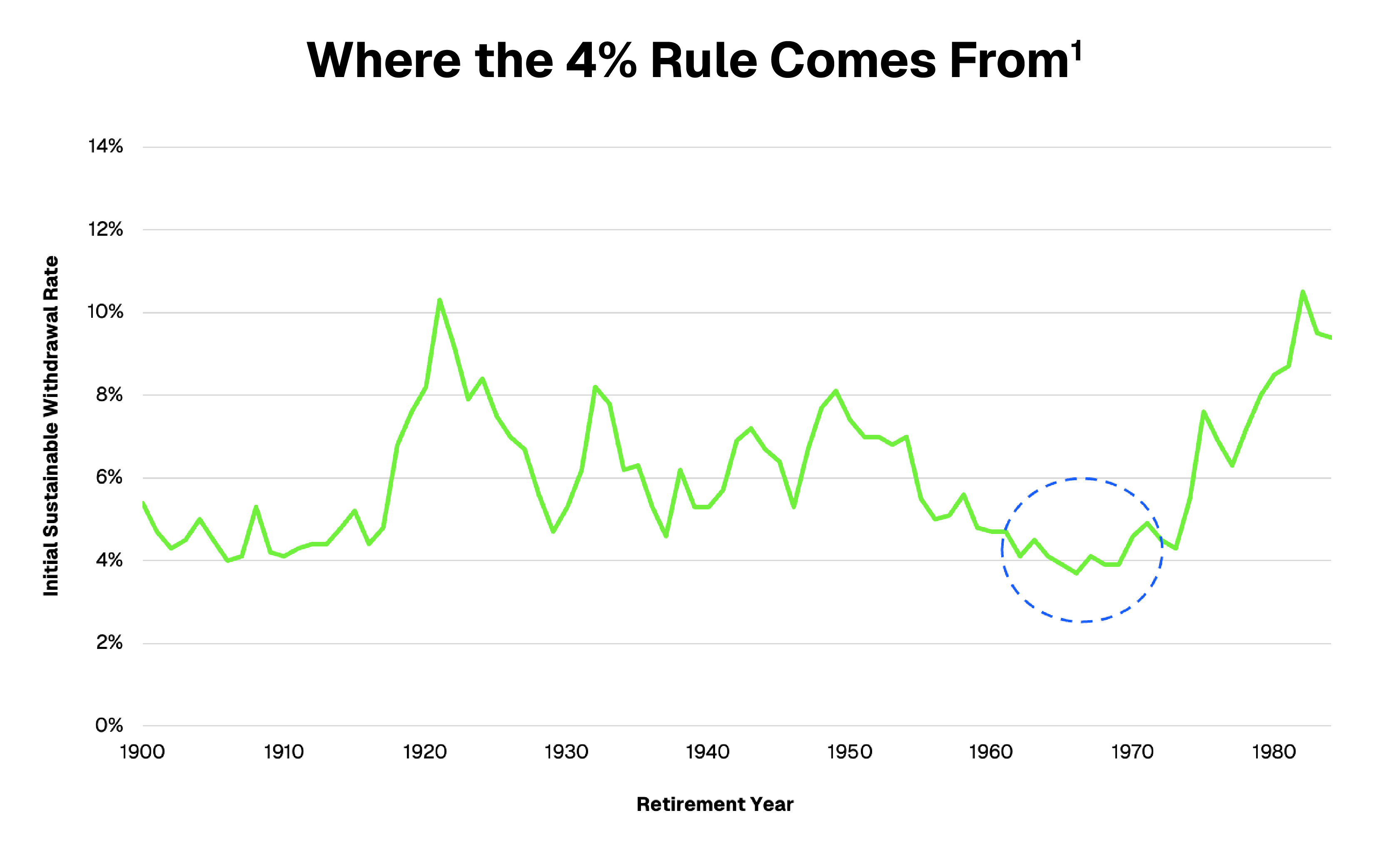

The 4% Rule was developed by financial planner William Bengen in 1994 as a guide for how much a retiree can safely spend from their investment portfolio each year in retirement without running out of money.

The goal of the rule is to ensure a steady stream of income that keeps up with inflation while preserving the longevity of the portfolio.

In its original form, Bengen’s rule suggested that retirees could withdraw 4% of their initial investment portfolio balance each year, adjusting for inflation annually, to support a 30-year retirement.

This assumes that a minimum of 50% of the portfolio is invested in stocks, with 75% being Bengen’s recommended allocation.

So, if you have $1 million in your retirement portfolio, you could withdraw $40,000 in the first year of retirement. In the second year, you could withdraw $40,000 + (2% * $1 million), or $40,800. And so on.

Challenges of the 4% Rule

The "safe” withdrawal rate has been hotly debated by experts for decades. Even William Bengen himself has revised the rule, raising his recommendation to 4.7% for all but worst-case scenarios, then cautioning retirees to spend less and reduce their equity exposure in this post-pandemic inflationary environment.

This highlights one of the biggest challenges of the 4% Rule. A significant downturn just before or soon after retirement could make it difficult if not impossible to continue applying the 4% Rule and make your money last throughout retirement.

CEO of DPL Financial Services, David Lau, says it’s fine to use the 4% Rule as a rule of thumb for portfolio withdrawals but it shouldn’t be used as a retirement income plan. Retirees need alternatives to the flawed guideline.

“It’s one thing to tell clients to swallow their worry and ride the market rollercoaster through retirement and it’s another thing entirely to do it,” says Lau. “The 4% Rule makes sense and, if nothing very unusual happens, you’ll be fine.”

But it can be difficult for a retiree to stick to a plan that relies on market performance during times of volatility.

Not every person is comfortable relying on their investments for income, so it’s important to address your tolerance for income risk before retirement begins, with planning that considers both financial and emotional needs.

The 4% Rule simply doesn’t work for everyone as a primary strategy for retirement income.

Learn about the basics of annuities and how they work.

Annuities vs. the 4% Rule

Annuities are products from insurance companies that offer a unique advantage in retirement planning by providing an income stream that is secure and predictable.

Unlike a portfolio drawdown strategy like the 4% Rule, annuities offer an income stream that is guaranteed to last as long as you do regardless of market performance.

For those who are uncomfortable depending on the markets and a portfolio withdrawal rate for retirement income, guaranteed income from an annuity can help alleviate fears about running out of money and provide protection from the potentially devastating portfolio impacts of a bear market early in retirement.

Through their structure, annuities manage risks and generate income in a way that can’t be achieved through investments. In fact, annuities uniquely address two of the biggest risks in retirement—longevity risk, or the risk of outliving your retirement savings, and sequence of returns risk, or the risk of a market downturn early in retirement depleting your portfolio to the point it is unable to support income withdrawals throughout retirement.

There are many types of annuities that offer a range of benefits in addition to income, including tax-deferred asset growth and asset protection. And now, modern annuities are available that are commission-free (also known as fee-based or no-load annuities).

These simplified products are built to deliver better consumer value with lower costs and improved benefits over their commissioned predecessors.

Annuities can also provide psychological benefits; having secure annuity income can help alleviate worries about market performance and income predictability. Because of their efficiency and stability, annuities should be considered as an option if you are not comfortable relying solely on your investments portfolio and a withdrawal framework like the 4% Rule for retirement income.

"Annuities manage risks and generate income in ways a withdrawal framework like the 4% rule cannot"

Learn how to use annuities in a financial plan.

Key Considerations for Sourcing Retirement Income

Individual Circumstances

When evaluating retirement income strategies, consider factors such as your retirement age, life expectancy, tolerance for income risk, and overall financial situation.

If you believe you will live a long time or are worried about market volatility impacting your investments, adding a source of guaranteed income like an annuity may be right for you.

Income Needs

When considering how to generate income, it is helpful to start by identifying how much income you will need to fund retirement spending.

It can be a smart strategy to cover your essential expenses with income from secure sources like a pension and/or an annuity. This ensures you’ll have funds for your most important needs and can give you more flexibility to invest the rest of your portfolio for growth and discretionary spending.

Learn more about the different types of annuities.

Inflation Adjustments

Inflation is a fact of life, and a retirement income strategy needs to consider the rising cost of living.

If you rely on your portfolio for income, inflation can be factored into your annual withdrawal rate, like the 4% Rule. With an annuity, there are options like a cost-of-living adjustment (COLA) that can help maintain purchasing power over the course of retirement.

"Inflation is a fact of life — ensure your retirement income plan includes the adjustments"

The 4% Rule is a very popular guideline for how to generate income from an investments portfolio over a 30-year retirement. However, for people who may not be comfortable relying on their investments alone to fund retirement spending, an annuity is a good option to consider.

With so many factors outside of our control that can impact retirement, including economic volatility, healthcare needs, and how long you will live, having guaranteed income from an annuity can provide peace of mind and income security.

It’s always wise to consult with a fee-only financial advisor to ensure that your income strategy aligns with your goals and needs for a successful retirement.

DPL has several tools to help you learn more about commission-free annuities and see how these solutions fit in a retirement portfolio.

[press-a-contact-location]

1 DMS data, return of 60% equity/40% bond portfolio, US stocks and US bonds, 1900-2020

.avif)