Harnessing the Power of Annuities in Your Financial Plan

Creating a comprehensive financial plan involves careful consideration of your financial goals and the appropriate strategies to meet them.

Whether you’re planning on your own or with a financial advisor, it’s important to understand the tools available to help you grow and protect your wealth before retirement and turn that wealth into income when you retire.

Annuities can be powerful tools in your financial plan and can help:

- Grow your assets while protecting them from market loss

- Take advantage of tax-deferral

- Generate guaranteed lifetime income

- Supplement Social Security and help protect against “longevity risk” (the risk of outliving your money)

Learn more about the basics of annuities and how they work.

What Makes Today’s Annuities Different

There are many misconceptions about annuities. Modern annuities deliver benefits their old-style, commission-driven predecessors couldn’t. Today, they are:

- Commission-free — Lower cost, more flexibility, consumer-focused

- More transparent — More understandable product costs and benefits

- Client-centered — Designed to support income, growth, and protection

Four Common Ways Annuities Are Used

1. Provide predictable, secure retirement income.

Annuities are insurance products designed to provide a guaranteed income stream for life. Annuities often are used to generate income for living expenses in retirement, ensuring a paycheck arrives at your chosen frequency, no matter how long you live.

2. Supplement Social Security.

Some worry that income from Social Security is not enough to live on during retirement. Annuities can be used to bridge the gap between your Social Security income and the amount you need to pay your monthly living expenses.

3. Leave a legacy.

Some annuities offer a “death benefit”, which means a beneficiary you choose receives a payout if you die before the annuity matures. In addition, when annuities are used to generate income for essential expenses, it frees up the rest of your portfolio to invest in a larger legacy.

4. Save on taxes.

Annuities can offer tax benefits, such as tax-deferred growth.

Steps to Evaluate Annuities in Your Financial Plan

Step 1: Consider your financial needs and goals

The financial planning process begins by identifying your goals and needs.

Think not just about your financial goals, but your emotional needs and preferences as well. Are you someone who is comfortable with risk, or do you prefer certainty? Is income security more important to you than asset accumulation? Is leaving money to your heirs a priority?

Depending upon your answers, you can determine a strategy with solutions that align with your needs and how an annuity can play a role.

Step 2: Research your options

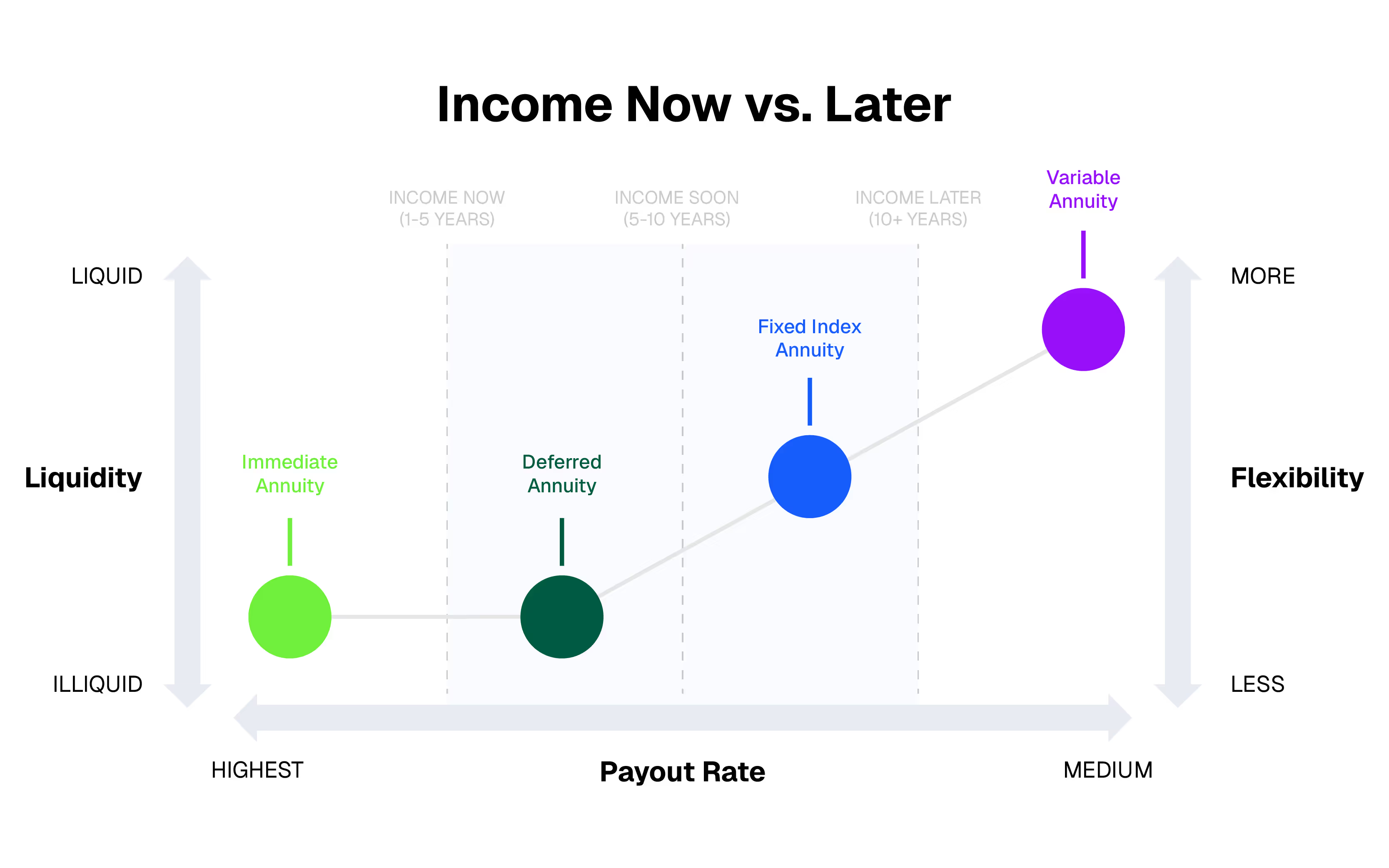

Annuities come in a variety of types that address a range of financial needs. A CD-like, fixed annuity can be used to grow and protect assets with a guaranteed interest rate; a variable annuity can provide greater growth potential with market exposure; a fixed index annuity (FIA) can provide tax-deferred growth with 100% downside protection.

When you’re ready, each type can turn your assets into income. Aligning the annuity types to your goals helps you understand which product may be right for you, and the benefits, like rising income, you will need.

Another important consideration is the insurance company that provides the annuity.

Insurance companies are rated based on their financial strength by four leading rating agencies. Many leading insurance companies offer annuities. Make sure you are comfortable with the company issuing the product you are considering.

Step 3: Understand the product costs

Annuities have costs, so it’s important to understand what you will pay for the product and the benefits you select before your purchase.

Today’s modern annuities are less expensive and less complex than the traditional, commissioned annuities that preceded them. Commission-free annuities do not have sales commissions in the pricing and typically are lower cost with greater flexibility and improved benefits for the consumer. You can find details on product costs in the fact sheets for fixed products and the prospectus for variable products.

Step 4: Talk to a fiduciary financial advisor

Not all financial advisors are willing to consider annuities for their clients. Seek guidance from a fiduciary financial advisor experienced in commission-free, or fee-based annuities. Have a conversation about your goals and whether an annuity is the right solution for accumulation, income, risk mitigation, or another need in your financial plan. Ask the advisor to show you the impact of an annuity on your plan and compare it to other solutions so you can make an informed decision.

Step 5: Determine how much to allocate to an annuity

How much you put into the annuity depends on your goal for the product.

When an annuity is being purchased for an income benefit, retirement researcher Wade Pfau recommends allocating a portion of your fixed income to the annuity, usually around 20% of your entire portfolio depending on the product and your needs.

There are free tools available at dplfp.com that enable you to quickly see how much it costs to generate a specific amount of income from a commission-free annuity. Work with a professional to determine the allocation that makes sense based on your goal and overall plan.

Step 6: Explore payout options

Annuities offer various payout options to suit your needs and preferences. Depending on the annuity, you can receive income in a lump sum or through a series of regular payments (there are tax implications with these choices).

You can turn on income immediately or defer income for many years to let your assets accumulate and earn a higher payout. Joint and survivor benefits are available to protect your spouse or partner by extending payments after your death. Select a product with payout options that align with your goals and understand the costs and conditions associated with these benefits.

Step 7: Understand tax implications

How you fund the annuity, with pre-tax (“qualified”) or after-tax (“non-qualified”) dollars, will impact your tax liability and payouts when you begin taking income. Consult with a tax advisor to understand how an annuity fits into your overall tax strategy and potential tax obligations on the assets.

Step 8: Review and monitor your financial plan regularly

Financial needs and goals can change over time. Review your financial plan at least annually to ensure your investments and strategy align with your goals. If you have an annuity with an income benefit, make sure you turn on income as planned. Many people don’t realize they need to request income to be turned on, otherwise the benefit goes unused. If you have an annuity with a benefit you no longer need, consider transferring the assets to another product that better meets your needs. A financial professional can help.

Many people do not realize annuity income benefits must be activated — they do not begin automatically. Reviewing your financial plan annually with your advisor helps ensure your income strategy stays on plan.

Annuities can be used to meet specific needs in a financial plan. Today, low-cost, commission-free annuities are available, offering guaranteed lifetime income, tax-deferred growth, asset protection, and other meaningful benefits. These modern annuities are less expensive and less complex than the traditional commissioned annuities that preceded them.

Before purchasing an annuity, it is important to compare product types, benefits, and costs to ensure the product you select is suitable for your goals and needs. A financial professional can help. When interviewing advisors, ask if they're a fiduciary and if they've ever used commission-free, or fee-based, annuities.

DPL has several tools to help you learn more about commission-free annuities and see how these solutions fit in a retirement portfolio. We can help.

[press-a-contact-location]

.avif)