No Matter What the Purpose of Your Wealth Is, Guaranteed Income Can Help You Realize It

Many Americans save for a dream retirement, but an equally important goal is to ensure essential expenses are covered. Without a clear understanding of what your savings need to accomplish, it's difficult to achieve a secure and fulfilling retirement.

Building a confident retirement plan begins by asking a fundamental question: What is the purpose of my wealth? A simple, three-step strategy can help you find the answer, defining what your savings must do for you, not just what you'd like them to do. This clarity offers a sense of security that empowers you to plan for other aspirations.

Here’s how it works:

Step 1: Determine Your Essential Costs

The first step is to calculate how much money you’ll need to cover basic, day-to-day living expenses in retirement. Start by reviewing your current expenses; some will continue into retirement and others will diminish or disappear when you stop working.

For example, if your home mortgage is paid off by the time you retire, that expense will be eliminated. However, you will still need to budget for home maintenance, insurance, and property taxes. Similarly, you may own your vehicle when you retire. While this means no monthly loan payments, you will still need to budget for insurance, gas, and maintenance.

A hypothetical annual budget for essentials for a retired couple might include:

- Housing = $13,700 (utilities, maintenance, insurance, property taxes for a $350,000 home)

- Food = $12,000 (groceries and dining out)

- Transportation = $8,900 (fuel, insurance, and maintenance for two owned cars)

- Healthcare = $14,400 (Medicare and supplemental insurance premiums, out-of-pocket costs)

Based on this example, the total annual budget for essentials at $49,000.1 When you multiply that by 30 years (or longer), it puts the financial reality of funding your retirement into perspective.

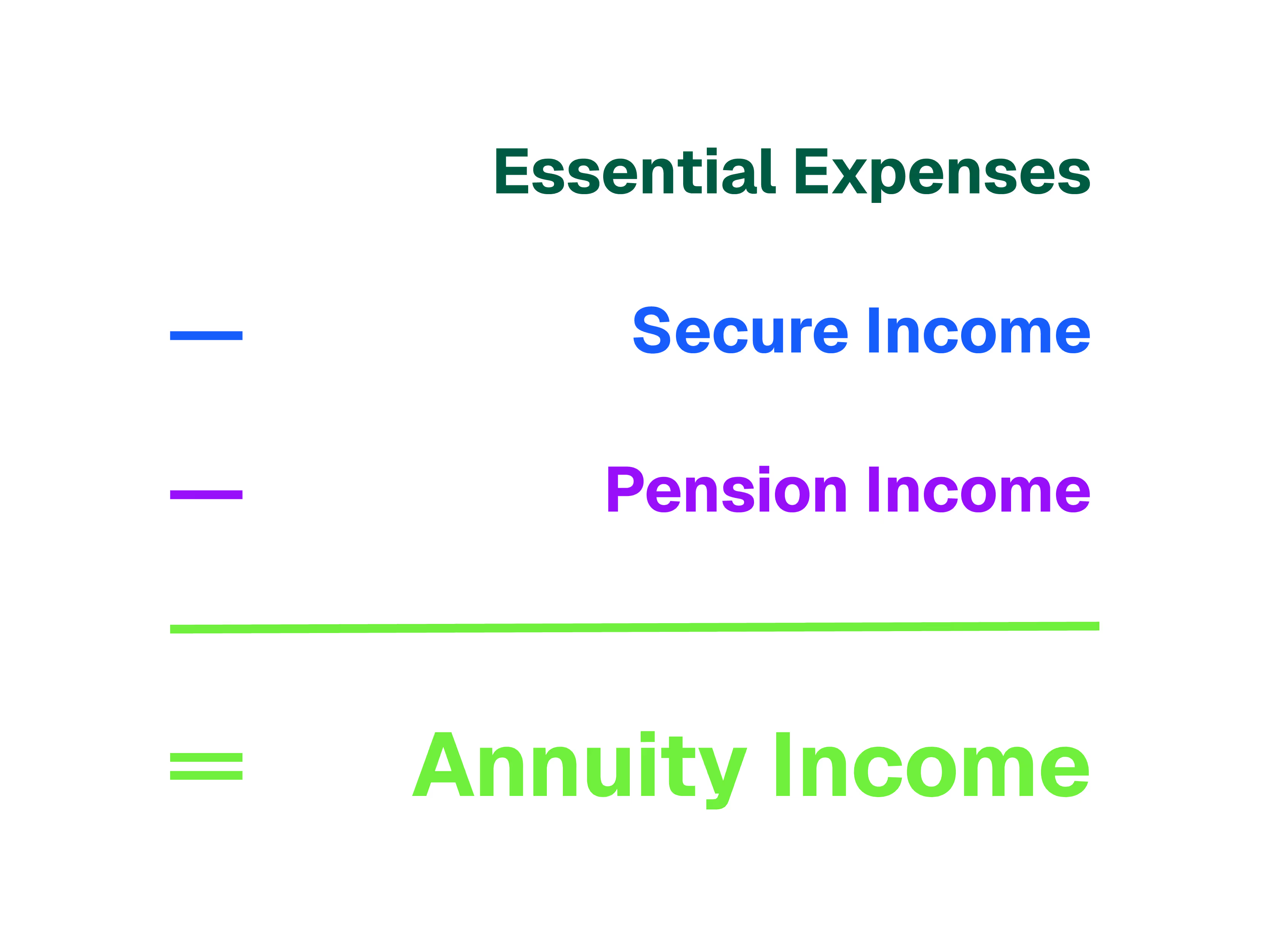

Step 2: Cover Expenses with Guaranteed Income Sources

At DPL, we explain that there are three primary sources of guaranteed income for retirees: pensions, Social Security, and commission-free annuities.

Employer-funded pensions have largely been phased out of the American workforce. Social Security is designed to support retirees but doesn't cover all retirement expenses, and the program's long-term viability is a frequent topic of debate.

The third source of guaranteed income is investing in a commission-free annuity. Many annuity owners view these products as a personal pension that provides a monthly retirement “paycheck” that they can’t outlive.

Commission-free annuities can be a smart choice for retirement because they deliver:

- Peace of mind. Your annuity can provide guaranteed income over your life and the life of your spouse

- Inflation protection. A cost-of-living rider will increase the income your annuity provides each year to help protect you from rising prices

- Income protection. Annuity payments remain steady, even when stock and bond markets are volatile

For many, guaranteed lifetime income provides a powerful sense of financial security, and acts as a crucial safety net. A 2024 survey of current annuity owners found that 97% said their annuities helped them worry less about running out of money, and 93% of annuity owners felt less anxious about their daily expenses.2

Some people can fund guaranteed lifetime income through annuities offered by their workplace retirement plans.3 Others may opt to fund the annuity by making multiple payments during their working years, or by rolling over assets from a 401(k) or an IRA at retirement.

It’s important to know that not all annuities are the same. Commission-free annuities are lower-cost, so they can deliver better value, more transparency, and often higher payouts than traditional commissioned annuities.

"Retirement isn’t the finish line; it’s the next leg of the race"

Step 3: Allocate for Discretionary Spending

Once the essential expenses are covered, you can decide what else your wealth should do for you in retirement and beyond. Whether it’s travelling, pursuing a new hobby, paying for a loved one’s education, or supporting a favorite cause, you can plan accordingly, knowing your retirement is secure.

Following this three-step strategy can help you build a more confident retirement plan. Having a secure source of guaranteed income that cannot be outlived can ease many of the financial challenges that come with retirement. It also allows retirees to invest and spend their portfolios in ways they might not otherwise, essentially granting permission to pursue the retirement of their dreams.

DPL has several tools to help you learn more about commission-free annuities and see how these solutions fit in a retirement portfolio.

[press-a-contact-location]

.avif)