Looking for Predictability in an Unpredictable World?

The risks associated with investment uncertainty and market volatility have been apparent this year. In April, the CBOE Volatility Index, often called Wall Street’s “fear gauge,” rose to a level it has only reached twice before. Those other times were the 2008 financial crisis and the coronavirus pandemic.1

Protection From Market Volatility

The heightened volatility of financial markets in 2025 has raised concerns among older Americans about whether they’ll be able to retire as planned and reinforced a cautious outlook of some younger investors.

In fact, a 2024 survey by the Employee Benefits Research Institute revealed that 83% of respondents were interested in using some of their retirement savings to purchase products delivering guaranteed income.2

For these groups, adding annuities to their asset allocation strategies can offer a measure of certainty and peace of mind. Commission-free annuities are uniquely designed to deliver protected growth and guaranteed lifetime income that stocks and bonds cannot.

Younger annuity holders know how these products will perform during the “accumulation” phase, when their money is growing tax-free inside the annuity. Likewise, retired annuity owners can count on a predictable stream of income during the “decumulation” phase, when the annuity begins making regular payouts. As a result, they don’t have to worry about the ups and downs in the financial markets, which can deplete a portfolio and hinder its ability to generate enough income to cover expenses in retirement.

Managing the Unpredictable

Here’s a little-known fact — Social Security is much like an annuity. Americans pay into the Social Security system and, in return, receive benefits – retirement paychecks, if you will – that they hope will provide steady and predictable income for as long as they live.

Modern, commission-free annuities act like personal pension plans that offer similar peace of mind by helping to improve financial outcomes in important ways.

Annuities can help contract owners manage the unpredictable risks associated with:

Turbulent markets.

Commission-free annuities are versatile tools. While they’re best known for delivering guaranteed income for life, they can do much more. When used strategically in a portfolio, annuities can deliver attractive returns, tax-advantaged growth, and principal protection.

For example, a stock market downturn just before or early in retirement can have a significant effect on how long retirement savings will last and how much income it will produce. Some annuities give owners the opportunity to participate in the performance of a stock market index, while reducing exposure to market losses. These annuities provide a measure of safety and predictability that stocks do not.

Longer-than-expected life.

Annuities offer guaranteed lifetime income. No one knows how long they’ll live, and that makes retirement income planning a challenge. A commission-free annuity can be used as a personal pension to help mitigate longevity risk by delivering guaranteed income payments for the annuity owner’s life – and the life of their spouse, if they choose that option.

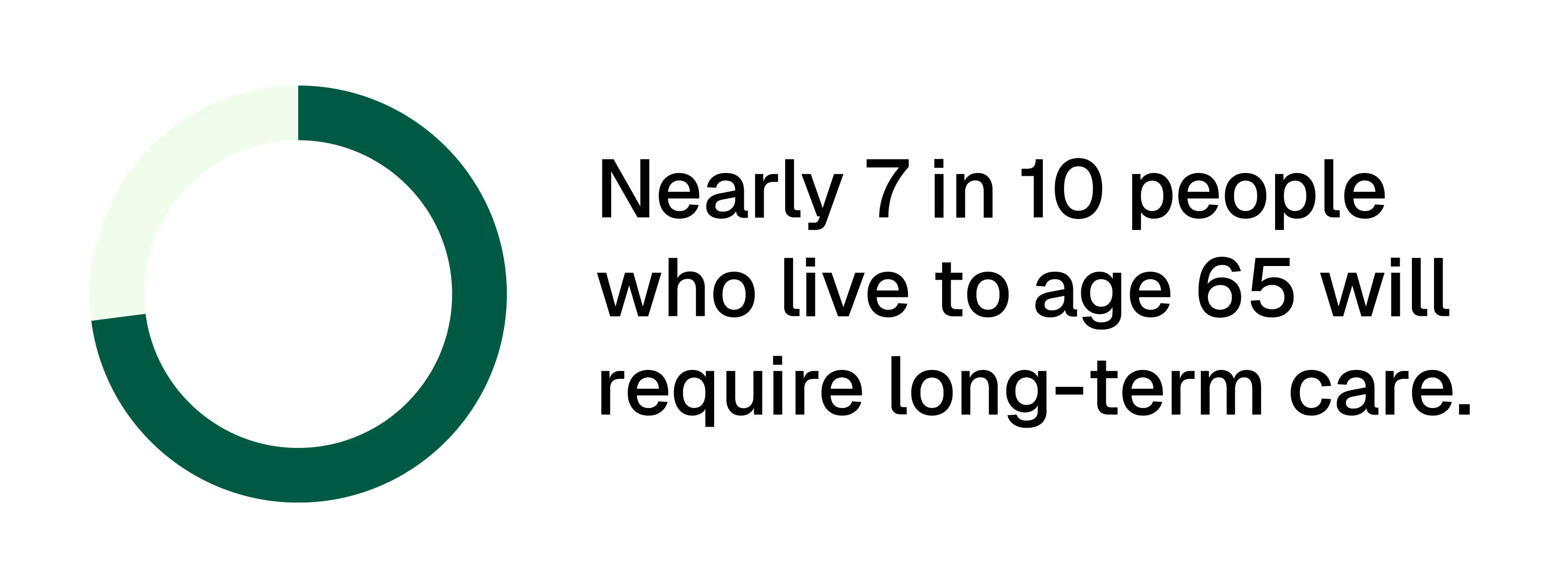

Long-term care needs.

Don't underestimate the need for long-term care (LTC). Nearly seven in 10 people who live to age 65 will require it.3 While LTC planning is an essential part of a comprehensive financial plan, the insurance can be costly, complex, and carry a “use it or lose it” risk if care is never required. One powerful solution is to purchase an annuity with an LTC rider. These riders allow annuity owners to access their annuity’s value to be used for qualified LTC expenses or provide enhanced care benefits, offering a more flexible approach to managing the potential financial impact of LTC needs.

Commission-free annuities are versatile. They’re predictable. And, today, you have access to a wide range of low-cost, commission-free annuities designed to protect and grow your assets and turn your nest egg into a stream of predictable income you can’t outlive.

In an unpredictable world, adding an annuity to your portfolio can add a measure of safety, confidence, and peace of mind.

If you would like to learn more about how commission-free annuities can help you achieve your financial goals in retirement, we can help.

[press-a-contact-location]

When evaluating the purchase of a variable annuity, you should be aware that variable annuities are long-term investment vehicles designed for retirement purposes and will fluctuate in value; annuities have limitations; and investing involves market risk, including possible loss of principal.

All guarantees based on the claims-paying ability of the issuing insurance carrier.

1 Nir Kaissar. “The Stock Market’s Fear Gauge Is Misunderstood" Bloomberg. May 6, 2025.

2 "The Misconception that Keeps People from Considering Annuities"

3 “Planning for Long-Term Care”

.avif)