The Difference Between a Broker-Dealer and a Financial Advisor

We all want our savings and investments to grow and help us accomplish our financial goals. Whether you want to buy a home, generate income, open a business, give to a good cause, help your children, or something else entirely, a financial adviser who understands your financial circumstances and what you want your money to achieve can make a difference in your success.

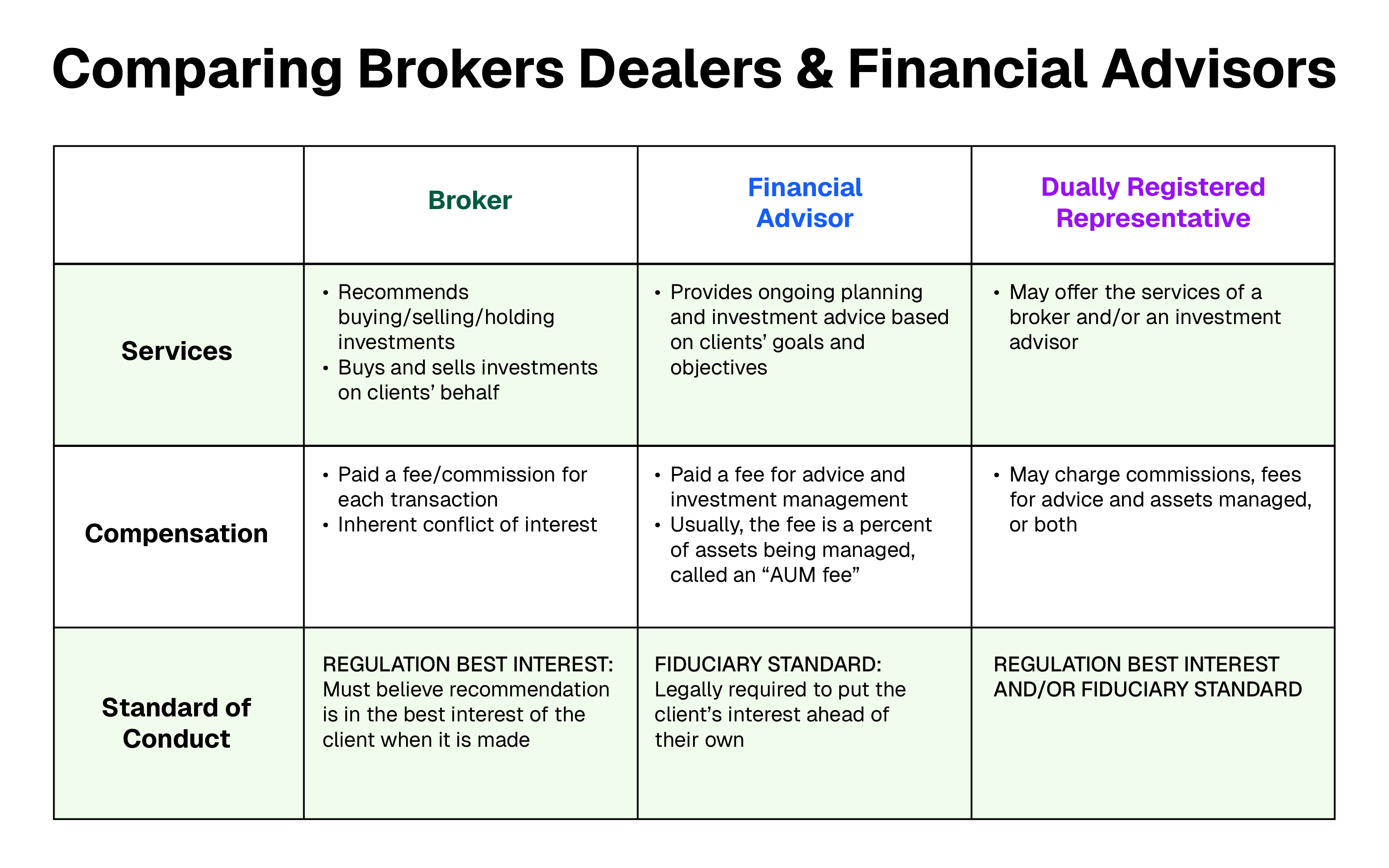

As you consider who to work with, make sure you clearly understand:

- The services the financial professional provides

- The way they will be compensated for their services

- The standard of conduct they follow

Here’s what you need to know:

What is a broker-dealer?

A broker-dealer is a firm or individual that buys and sells securities, such as stocks, bonds, and other investments.

When acting as a “broker,” they facilitate securities trades between two outside parties. When acting as a “dealer,” they buy for or sell from their own inventory of securities.

Type of broker-dealers include:

- Large national broker-dealers (e.g. Morgan Stanley, Bank of America Merrill Lynch) that create and sell investment products.1

- Independent broker-dealers that do not have proprietary investment products. They may be part of a larger firm (e.g. LPL Financial) or operate independently, buying and selling investments through the independent broker-dealer.2

Most brokers and dealers are required to register with the Securities and Exchange Commission (SEC), join a self-regulatory organization such as the Financial Industry Regulatory Authority (Finra), and register with state regulators.

Is there a difference between brokers and financial advisors?

Yes. The financial professionals who work for broker-dealers follow different business models.2 As a result, it’s imperative for people who are seeking financial assistance to ask questions and clearly understand how the financial professional operates.

Usually, people who work for broker-dealers fall into one of three categories:

1. Broker-dealer representatives (brokers) serve the interests of their broker-dealers, as well as those of their clients. The services provided may be more transactional and time specific.

Broker-dealer representatives usually:

- Make recommendations to buy, sell, or hold investments, including recommending the broker-dealer’s investment products

- Buy and sell investments at their clients’ discretion

- Earn fees and commissions on investments that are bought and sold. This can create a conflict of interest, as the representatives may be incentivized to prioritize financial gain if investments with different commission structures provide the same benefit to a client.

- Adhere to Regulation Best Interest (Reg BI), which requires advisors to have a reasonable basis to believe that each recommendation they make is in the best interest of the client at the time it is made.2

2. Financial advisors provide financial planning and advice, portfolio management, and other services.3 They typically do not sell products to clients for a commission.

These advisors usually:

- Develop a plan to help the client toward their financial goals

- Manage investments on behalf of the client

- Monitor plan progress over time

- Earn a fee for financial advice and portfolio management services, often it is a percentage of assets managed, called an AUM fee

- Adhere to a Fiduciary Standard that legally obligates them to place their clients' interests ahead of their own. This is a higher standard of conduct that demands complete transparency, conflict-of-interest avoidance, and unbiased guidance. Financial advisors who are fiduciaries are accountable for their recommendations and actions. Any breach of this duty can have legal consequences.4

"Fiduciaries are legally obligated to put their clients’ interests ahead of their own"

3. Dually registered representatives are broker-dealer representatives (compensated with commissions and subject to Reg BI) AND financial advisors (earning fees for advice and subject to the fiduciary standard).

About half of the representatives at broker-dealers are dually registered.5

If the financial professional you are interviewing is dually registered, ask:

- What services will you provide? You need to know whether they will always be acting as a fiduciary or whether they will sometimes act as a broker-dealer representative

- How will you charge? Will the representative earn commissions or fees for financial advice?

- What standard of care will govern your actions? Early in 2023, the SEC warned dually registered representatives that they must clearly communicate whether they are acting as clients’ brokers or advisors or a combination of the two.6

Should you choose a broker or financial advisor?

There are significant advantages to working with a financial advisor who is a fiduciary:

- Transparent fee structure — no commissions tied to product sales

- Legally required to act in your best interest

- Ongoing financial planning and accountability

One way to find out whether your financial professional is acting as a fiduciary is simple: ask.

The client services agreement should reflect the answer your financial professional provides.

And, if you have questions, we can help.

[press-a-contact-location]

1 The Role of Wirehouses And National/Regional Broker-Dealers In A Growing Financial Planning Profession. CFP Board. September 9, 2022. Cited December 4, 2023.

2 Staff Bulletin: Standards of Conduct for Broker-Dealers and Investment Advisers Care Obligations. U.S. Securities and Exchange Commission. Cited December 4, 2023.

3 Investment Advisers, FINRA. Cited December 4, 2023.

4 Staff Bulletin: Standards of Conduct for Broker-Dealers and Investment Advisers Conflicts of Interest. U.S. Securities and Exchange Commission. Cited December 4, 2023.

5 2023 FINRA Industry Snapshot. FINRA. Cited December 5, 2023.

6 Jake Martin. SEC Puts Dual-Registered Advisors on Notice in Risk Alert. Advisor Hub. January 30, 2023. Cited December 5, 2023.

.avif)