Navigating Sequence of Returns Risk

Key Takeaways

- Sequence of returns risk is the danger that a market downturn at the start of retirement can permanently damage your portfolio.

- The "fragile decade" — the five years before and after retirement — is the most critical window for the success of a retirement portfolio.

- Withdrawing from a declining portfolio accelerates losses, making recovery much harder than for an investor who hasn't yet started withdrawing.

- Strategies like maintaining a cash buffer, building a guaranteed income floor, and using fixed index annuities can significantly reduce this risk.

- Commission-free unities offer low-cost, transparent tools to balance growth and protection when it matters most.

While most investors focus on average annual returns, the order in which those returns occur matters much more as you approach retirement. This phenomenon is known as sequence of returns risk.: the chance that a market downturn just as you begin or are about retire could have a detrimental impact on your portfolio that could take years to recover.

What is the Fragile Decade?

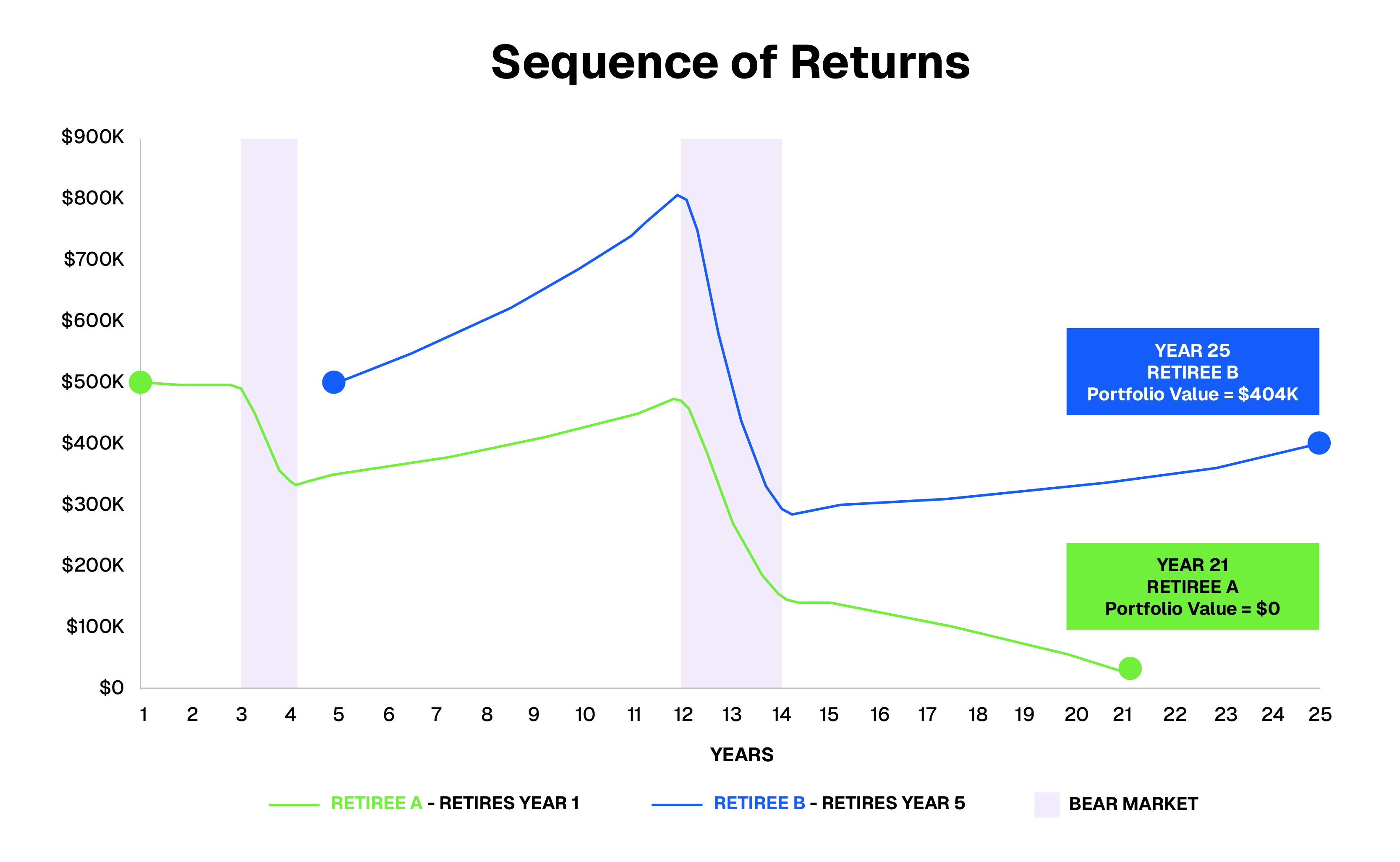

The most critical window for your portfolio is the fragile decade: the five years before and after retirement. During this time, a combination of poor market performance and portfolio withdrawals could have a devastating effect on your retirement nest egg.

To illustrate, let’s look at two fictional retirees, Jack and Jill, who both started with $500,000:

- Jack retired during a market downturn. Because he had to sell assets at a loss to generate income, his portfolio was completely depleted after 15 years.

- Jill retired four years after the market downturn, just as it was starting to rise. Fifteen years into retirement, the value of her portfolio is higher than when she first retired.

Implementation Insight

The difference between Jack’s and Jill’s outcomes wasn’t their average return — it was timing. Jack’s portfolio never recovered because early withdrawals locked in losses during the downturn. Jill’s portfolio benefited from compounding gains before withdrawals began.

Mitigating the Risk

Since it is impossible to predict market performance, you need a strategy that limits the impact of volatility on your retirement income.

- Maintain Ample Cash: Keeping one or two years of living expenses in cash or high-yielding fixed annuities reduces the need to sell stocks at a loss during a down market.

- Build a Predictable Income Floor: Using commission-free annuities to create guaranteed lifetime income can ensure your essential expenses are met regardless of market performance. This helps you resist the urge to sell assets when markets are low.

- Participate with Protection: Fixed index annuities (FIAs) allow you to benefit from stock market gains while providing complete protection from market losses. They are a powerful alternative to bonds, especially when both stocks and bonds are underperforming.

Balance Growth and Protection

A well-designed retirement plan doesn’t just focus on growth. It balances growth and protection against risks like market volatility, especially near or early into retirement. Commission-free annuities are designed for this balance, offering low-cost, transparent ways to safeguard your lifestyle.

To learn more about protecting your portfolio against the risk of outliving your savings, read DPL’s post on Longevity Risk or download our free Retirement Income Planning Guide to start strengthening your strategy today.

[press-a-contact-location]

.avif)