Understanding and Managing Longevity Risk

Key Takeaways

- Longevity risk is the possibility of outliving your retirement savings — a real challenge as life expectancy continues to rise.

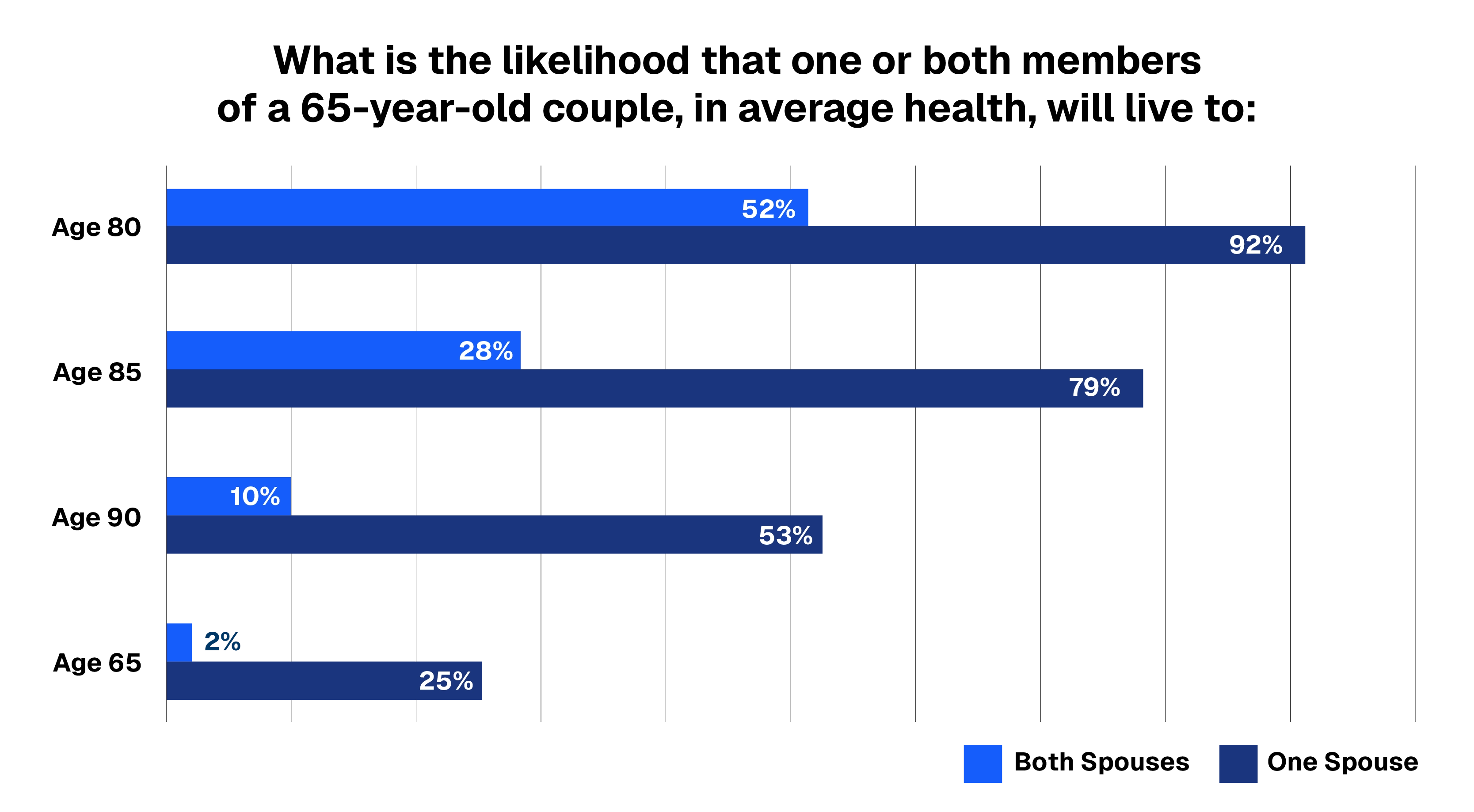

- Many people underestimate their planning horizon; for a 65-year-old couple, there is a 53% chance at least one spouse will reach age 90.

- Modern, commission-free annuities offer strategies like income floors, Social Security bridging, and longevity insurance to help manage this risk.

- Annuities can also provide protection against cognitive decline by offering a steady, automated income stream.

- Comprehensive Strategy combines guaranteed income sources, Social Security optimization, and commission-free annuity solutions.

Retirement is a time of excitement, but it also brings unique uncertainties. One of the most significant challenges you may face is longevity risk — the real possibility of outliving your retirement savings.

Why Longevity is a Risk

Planning for retirement is a bit like planning a long vacation; you have to prepare for the unexpected to ensure your trip isn't derailed. Many people unfortunately underestimate their planning horizon by looking only at average life expectancy at birth, which is currently around 76 years in the U.S.

However, the longer you live, the longer you are likely to continue living. For a 65-year-old couple in average health, there is a 53% chance that at least one spouse will reach age 90, and a 25% chance one will reach age 95. Without a strategy to address this "extra" time, you run the risk of exhausting your retirement savings.

Strategies to Safeguard Your Savings

Modern, commission-free annuities offer several ways to minimize longevity risk and provide peace of mind:

- Create an "Income Floor": Cover your essential, day-to-day expenses with guaranteed income from secure sources like Social Security and annuities.

- Bridge the Social Security Gap: By 2034, Social Security benefits may be reduced by 20–25% unless the government acts. Annuities can help fill this potential gap.

- Purchase Longevity Insurance: You can use annuities to begin receiving income at a later age, such as 85, ensuring you have funds in your later years.

- Maximize Social Security Benefits: If you want to delay Social Security until age 70 to receive 124% of your benefit, annuities can provide the necessary bridge income during your 60s.

Cognitive Decline: Protecting Your Retirement

Living longer also increases the risk of cognitive decline, which poses a significant threat to financial well-being in retirement. As we age, decision-making abilities can deteriorate, possibly leading to money mismanagement or vulnerability to fraud.

Commission-free annuities can help mitigate the financial risks associated with cognitive decline. An annuity purchased early in retirement may offer some de facto protection against fraud, which could discourage scammers seeking fast money to move along. In addition, annuities can be customized to help offset the costs of long-term care.

To strengthen your full retirement income strategy, download our Retirement Income Planning Guide.

[press-a-contact-location]

.avif)