A Guide to Estimating Retirement Expenses

.webp)

Successful retirement plans don’t start with how much you have but understanding how much you’ll spend

Many Americans diligently save for retirement, but they overlook a crucial question: How much will I spend in retirement? Without some understanding of retirement expenses, it’s nearly impossible to determine:

• If you are saving enough

• When can you afford to retire

• Your investment risk tolerance

While estimating retirement expenses isn’t an exact science, it is a vital step to avoid a retirement income shortfall.

What are retirement expenses?

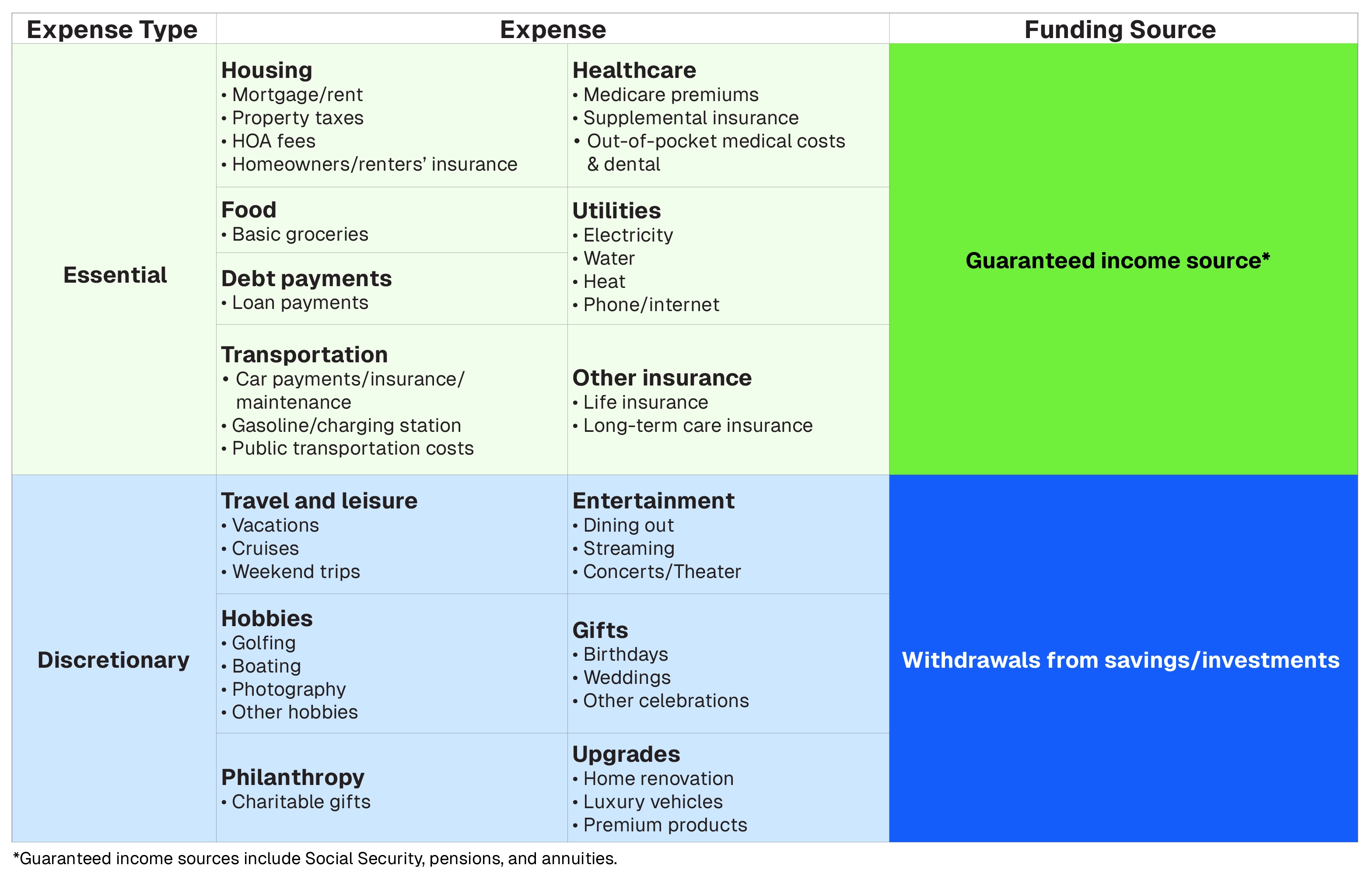

Basic living costs for housing, food, and other essentials remain in retirement while other expenses can fluctuate. For example, commuting costs and payroll taxes typically vanish after retirement, but healthcare and discretionary spending on travel or hobbies will likely increase.

To simply your retirement financial planning, divide your budget into two categories:

• Needs: Essential expenses (housing/utilities, healthcare, insurance) should be covered by guaranteed income sources, such as Social Security, pensions, and annuity insurance products.

• Wants: Discretionary expenses (vacations, hobbies, philanthropy) can be covered based on investment portfolio performance.

Two ways to estimate retirement costs

There is no “right” way to estimate retirement expenses, but these two approaches each have advantages and limitations.

Build a custom retirement budget

The most accurate way to estimate retirement expenses is to determine how your current spending will need to be adjusted for your future lifestyle.

• Analysis: Review bank and credit card statements to identify your current spending.

• Adjust: Factor in anticipated life changes. For example, household costs may drop once children leave home and become financially independent, but travel expenses may rise if they live far away.

• Categorize: Designate each expense as a “need” or a “want.”

Use an income replacement ratio

An alternative method is to assume you’ll need 70% to 90% of your pre-retirement income to live comfortably in retirement.

• The Logic: Retirees typically spend less because they no longer have certain expenses. For example, eliminating payroll taxes (7.65%) and retirement contributions (10%–15%) can reduce your income needs by roughly 15%–20%.

When estimating retirement expenses, it’s important to keep in mind that spending changes in retirement can vary widely depending on your health, lifestyle goals, and financial factors, including income and debt.

Funding your retirement

Once you have an estimate of your retirement expenses, the next step is to identify income sources. Most retirees rely on a combination of these five sources:

• Social Security: Provides inflation-adjusted income for life. On average, Social Security payments replace 40% of pre-retirement earnings. Note: this percentage is higher for low earners and lower for high earners.1

• Pensions: Employer-provided benefits that offer predictable income paychecks for life. However, pensions have become rare, with just 15% of U.S. workers having access to pension plans through work as of March 2024.2

• Savings and investments: These assets, such as 401(k)s, IRAs or brokerage accounts, provide variable income. These sources will fluctuate based on market performance.

• Part-time work: Many retirees supplement their early years of retirement with bridge jobs to reduce the changes of depleting an investment portfolio.

• Annuities: An annuity can function as a personal pension that you purchase with a lump sum or a series of payments to provide a predictable, contractually guaranteed income stream for life.

Some individuals—particularly early retirees—use an annuity to cover essential expenses during the gap between retirement and the start of their Social Security benefits. Annuity income payouts can begin right away or be deferred to a future date of your choosing, providing a reliable income stream that helps ease the financial concerns often associated with retirement.

How will inflation affect retirement expenses?

Inflation can significantly increase your retirement expenses over time. For example, if you retire at age 65 with a $50,000 annual budget, you will need close to $82,000 by age 85 just to maintain the same lifestyle, assuming a 2.5% average annual inflation rate.3

The good news is Social Security includes automatic cost-of-living adjustments, or COLAs, to keep pace with inflation. Annuities with rising income features and a diversified stock portfolio can help your income keep pace with rising prices.

Planning is an ongoing process

Retirement planning is most effective when expenses lead to the conversation, and savings and income considerations follow. By estimating your future costs now, you gain a clearer picture of how much to save, when you are financially ready to retire, and how to balance your future needs and wants.

Remember, a retirement plan shouldn’t be managed with a “set it and forget it” approach. It is a living strategy that should be reviewed annually and especially after major life events, such as changes in health, receiving an inheritance, or a shift in family circumstances.

Disclosures:

1 Peter G. Peterson Foundation. “Social Security Reform: Options to Adjust Benefits. April 24, 2025

2 U.S. Bureau of Labor Statistics. “TED: The Economics Daily.” June 4, 2025.

.avif)